If you’re thinking about diving into the world of rental properties in 2026, my honest answer is: yes, it absolutely can be a right time, provided you approach it smartly and strategically. The market might not be screaming hot like it was a few years ago, but that’s actually what makes it interesting and potentially rewarding for the right kind of investor.

I know, I know. The headlines can be a bit confusing. Some say prices are too high, others talk about rents cooling down. But when I look at the bigger picture, I see a market that’s settling into a more balanced rhythm, creating opportunities for those who are patient and informed. It’s not about chasing quick flips; it’s about building long-term wealth by providing a fundamental need: a place for people to live. And right now, that need is strong, even with some shifts happening.

Is 2026 the Right Time to Invest in Real Estate Rentals?

Let’s break down what’s going on right now, in mid-2026. The days of bidding wars and skyrocketing rents seem to be on pause, and that’s mostly due to a bit more supply hitting the market. We’re seeing vacancy rates tick up a little, reaching about 7.3% nationally in the first quarter of 2026. This is the highest we’ve seen in a few years, especially in big apartment buildings in the South and West, where a lot of new construction wrapped up in 2024 and 2025.

What does this mean for rents? Well, effective asking rents for apartments have seen a slight dip, maybe around 0.5% to 1.7% lower than last year, with the national average sitting somewhere between $1,370 and $1,672.

But here’s the crucial part: this wave of new building is slowing down sharply. Projections show significantly fewer apartment buildings being completed in 2026 and 2027. This is good news for investors because it means the extra supply won’t last forever. We’re likely to see vacancies stabilize and rents start growing again, maybe by a modest 0.5% to 2% for the year.

Now, single-family homes (think houses you’d rent out) have been a bit more steady. Rent growth for these has been holding strong, around 1% to 2% in many areas.

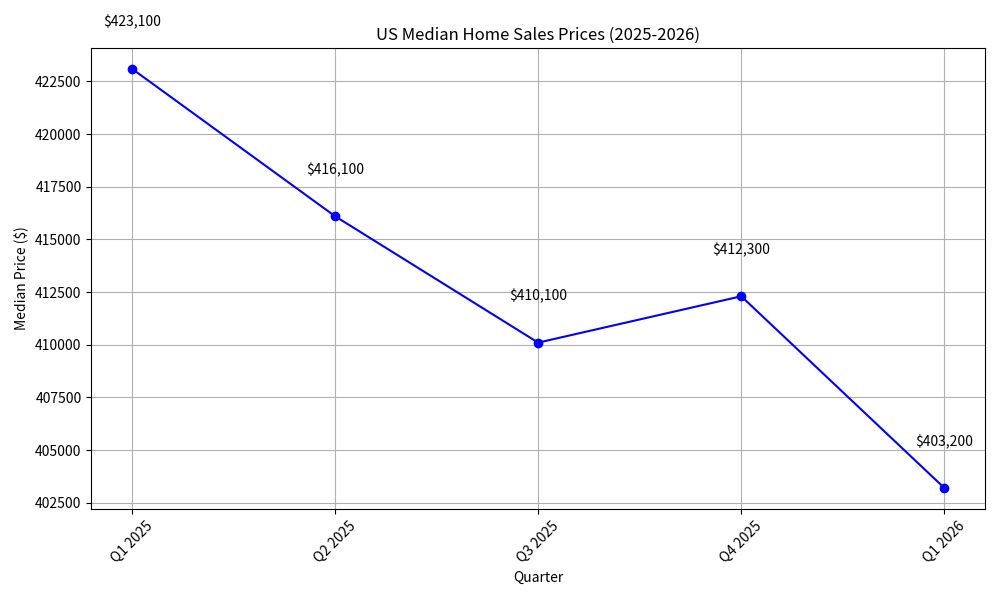

And what about home prices? They’re not zooming up like they used to, but they’re still high. The median home price is hovering around $403,000 to $425,000, and forecasts suggest they’ll stay pretty flat or grow very slowly, maybe 0% to 3.2% nationally.

US Median Home Sales Prices (Q1 2025 – Q1 2026)

| YEAR/QUARTER | MEDIAN PRICE RANGE |

|---|---|

| Q1 2025 | Elevated |

| Q1 2026 | $403,000 – $425,000 |

This environment really favors investors who are focused on cash flow – making money from the rent itself – rather than just hoping the property’s value will skyrocket. Plus, with home prices still high and mortgage rates a bit higher than we’re used to, more and more people are finding that renting is the more affordable option. That means steady demand for rentals for the foreseeable future.

The Economic Picture and How You Can Finance Your Investment

Let’s talk about money. Mortgage rates for a 30-year fixed loan are sitting around 6.3% to 6.4% as of mid-2026. Experts think they’ll stay in the mid-6% range, maybe dipping a bit to around 5.9% to 6.2% by the end of the year. While that’s not the super-low rates we saw a few years back, it’s definitely manageable for smart investors.

The overall economy is looking pretty stable. We’re seeing about 2.2% GDP growth, unemployment around 4.5%, and inflation cooling down. Job markets are strong in places like the South and Midwest, which is great news for attracting renters.

Now, when you’re looking to buy a rental property, the loans might be a little pricier than for your own home, often in the 7% to 8% range. That’s why focusing on cash-on-cash return – the profit you make relative to the cash you put down – is super important.

Understanding Rental Yields, Cap Rates, and Cash Flow

This is where the math gets exciting. Cap rates (capitalization rates, which help you figure out the potential return on a property) for apartment buildings are averaging around 5.8% nationally. That’s pretty stable and competitive.

For investors focused on individual properties, gross rental yields in good markets can be anywhere from 7% to 12%. After you factor in all your expenses – like mortgage, taxes, insurance, maintenance, and periods when the property is empty (vacancy) – you can often still see net yieldsof 4% to 7%.

Let me give you a quick example of how this could look in mid-2026:

Imagine you buy a $300,000 single-family home in a Midwest market. You put down 25% ($75,000). The monthly rent is $2,000 (that’s about an 8% gross yield). After your mortgage payment (let’s say around $1,300 at a 7.5% interest rate), property taxes, insurance, maintenance, and accounting for some vacancy, you might be looking at a net cash flow of $300 to $500 per month. And that’s on top of building equity and potential appreciation, not to mention the tax benefits!

Top Markets for Rental Investments in 2026

Location, location, location! It’s always true. I’ve noticed that Texas and Florida continue to be strong contenders, with ten of the top fifteen markets. Why? No state income tax, booming job and population growth, and landlord-friendly rules are big draws.

For immediate cash flow, some Midwest cities really shine. Here are a few I’m keeping an eye on:

- Indianapolis, IN: You can find high gross yields (around 9%), low vacancy rates, and the initial cost of buying is more affordable.

- Cleveland, OH: Offers fantastic cash flow (yields up to 11%) and has a steady economy thanks to healthcare and education.

- Buffalo, NY: Good yields (around 8%) and seeing people move in from more expensive parts of the Northeast.

- Durham, NC & Austin, TX: These are growth areas with solid rental demand, but it’s important to watch how quickly new apartments are being built and absorbed.

- Dallas-Fort Worth, Charlotte, Atlanta, Tampa: These offer a good balance of potential appreciation and rental demand.

On the flip side, I’d be more cautious in areas that have a lot of new construction already (making them potentially oversupplied) or places with high insurance costs, like parts of Florida and coastal Texas. Also, be aware of areas with strict local regulations.

The Upside: Why Rentals Make Sense Now

Even with the current market shifts, the long-term case for rental properties is incredibly strong.

- The Housing Shortage is Real: We’re facing a multi-million-unit deficit in housing across the country. New construction simply can’t keep up quickly enough.

- Hedge Against Inflation: Historically, rents and property values tend to rise along with inflation, helping your money hold its value.

- Tax Advantages: This is a big one! You can benefit from depreciation, deducting mortgage interest, a 20% Qualified Business Income deduction (which is now permanent!), and even deferring taxes when you sell and reinvest through 1031 exchanges.

- Leverage and Cash Flow: Using other people’s money (the mortgage) to build wealth is a powerful concept. Positive cash flow, especially in markets with good yields, can steadily grow your wealth over time.

- Demographics are on Your Side: Millions of Millennials and Gen Z are entering their prime renting years, and more higher-income households are choosing to rent by choice, not just necessity.

Risks and Challenges to Keep in Mind

Of course, no investment is without its risks. It’s important to be aware of them:

- Short-Term Rent Pressure: In some cities, higher vacancies might mean it takes a little longer to start seeing positive cash flow.

- Rising Operating Costs: Insurance premiums have gone up significantly, especially in areas prone to natural disasters. Property taxes and general maintenance costs also eat into profits.

- Interest Rate and Liquidity Risk: If interest rates stay higher for a long time, it could be more expensive to refinance or sell your property.

- Local Regulations: Rules about rent control, evictions, or short-term rentals vary greatly by city and state, and can impact your returns.

- Tenant and Management Issues: Dealing with vacancies, repairs, or difficult tenants can be a headache. Professional property management (which typically costs 8-10% of the rent) can be a worthwhile expense.

Your Practical Steps for Investing in 2026

So, how do you actually get started?

- Run the Numbers – Seriously: Don’t skip this! Look for properties where the monthly rent is at least 1% of the purchase price (the “1% rule”), or target properties with cash-on-cash returns of 8-10% or higher.

- Choose Your Property Wisely: For beginners, single-family homes or small multifamily properties (2-4 units) are usually the best starting point. As you gain experience, you can look at larger apartment buildings.

- Get Your Financing Lined Up: Shop around for loans specifically for investment properties. Credit unions and portfolio lenders can sometimes offer competitive rates.

- Build Your Team: You’ll need a good real estate agent who understands investors, a reliable property manager, a thorough inspector, a knowledgeable accountant, and an insurance broker who gets rental properties.

- Focus on Fundamentals: Always prioritize markets with strong job growth, population increases, low unemployment, and reasonable insurance and tax rates.

- Think Long-Term: 2026 is for buy-and-hold investors. Be prepared to weather any short-term dips and focus on the long-term gains.

The Bottom Line for 2026

In my opinion, yes, 2026 presents a compelling opportunity to invest in real estate rentals for the prepared and strategic investor. The current market softness, with its higher vacancies and more stable rents, could be a fantastic buyer’s window before supply tightens and rents start to rebound. When you combine this with moderating interest rates, consistently strong demand, and those valuable tax benefits, it creates an attractive entry point for building wealth over the long haul.

The key to success here is discipline. You need to buy in markets that will give you positive cash flow from day one, be conservative in your financial planning, keep a healthy reserve fund, and always think in terms of decades, not just months. Investors focusing on Midwest markets or specific Sun Belt areas with solid yields are particularly well-positioned for success.

The numbers are clear: the housing shortage isn’t going away anytime soon, and millions of Americans will continue to need good rental housing. If you do your homework, act thoughtfully, and focus on the fundamentals, you could set yourself up with a strong, inflation-protected income stream for years to come. The door is open, but you need to be ready to walk through it with a plan.